Tax Repercussions of Divorce

Tax Repercussions of Divorce

The worst time in your life is when you face a divorce. All logic flies out the window. Emotions rage and rule. Nobody gets a fair deal. There are a million stories—and you probably know many of them personally.

Setting emotions aside for the moment, let’s look at tax repercussions that will affect you if you and your spouse divorce

First, the good news:

1. If you divorce, you can split up all the assets you own together without any immediate tax consequences. There are no capital gains issues for splitting up the equity in homes, bank accounts, savings bonds, coin collections, artwork, etc.

2. You can get half the money in your spouse’s retirement plans by using a QDRO—that’s a court-ordered split.

3. You can keep living in your home while your children grow up—and still have each spouse get the benefit of your full $250,000 personal residence exclusion when you sell the house 10 years later.

Now the bad news:

1. If you have to sell stocks to split up the account, there will be capital gains taxes to pay. However,

- You might find yourself in a 0 percent or 15 percent capital gains bracket. That would be good.

- If your stocks are in “street name” rather than your name, you may be able to transfer stocks from your joint account or spouse’s account to your own account without actually selling the stocks.

2. If your stock sales show high losses when you cash out, your deductions for your losses will be limited to $3,000 per year over any gains you have each year.

3. If you split up the funds in your spouse’s IRAs by cashing them out, you will have to pay taxes on the withdrawals. There may even be penalties from the IRS and your state for drawing the funds before you are age 59½.

4. If you split up ownership of real estate, other than your home, you may face property tax increases. To avoid that, find out if your property tax collector has provisions to transfer title tax-free between spouses.

A Nasty Divorce Secret Revealed!

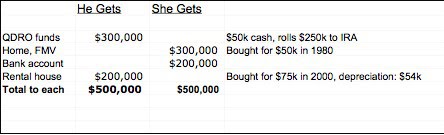

Beware! A clever attorney can split up your assets so both of you get the same fair market value—while only one of you ends up paying a fortune in taxes. How?

This looks even, right? Hardly!

In this scenario, the wife will end up with $500,000 worth of assets that come to her without any tax consequences.

In this scenario, the wife will end up with $500,000 worth of assets that come to her without any tax consequences.

The husband pays tax immediately on the $50,000 cash from the QDRO (without any early withdrawal penalties). He will pay taxes whenever he draws the other $250,000 from the QDRO—plus potential early withdrawal penalties. The rental house, when sold, will generate 25 percent federal taxes on the $54,000 depreciation (plus state taxes), along with long-term capital gains taxes on about $125,000 worth of gain (less selling costs of about $15,000).

Net effect? The husband really gets at least 25 percent less net value than the wife.

See how important it is to understand the underlying information before accepting a divorce settlement? When you’re informed, you can arrange a fair split.

Be sure to talk to a knowledgeable tax advisor who can help your divorce attorney think through the tax repercussions of the division of your assets.

Eva Rosenberg, EA is the publisher of TaxMama.com, where your tax questions are answered. Eva is the author of several books and ebooks, including Small Business Taxes Made Easy. Eva teaches a tax pro course at IRSExams.com.

Read More:

Phantom Income from a Short Sale or Foreclosure? TaxMama Gives You Two Ways to Avoid the Tax

New Tax Increase for Wealthy Americans: Will You Pay More?

Tax Tips for Commercial Real Estate Owners

Hiring? Do Your New Hires Qualify You for Tax Credits?